Weekly Market Recap:

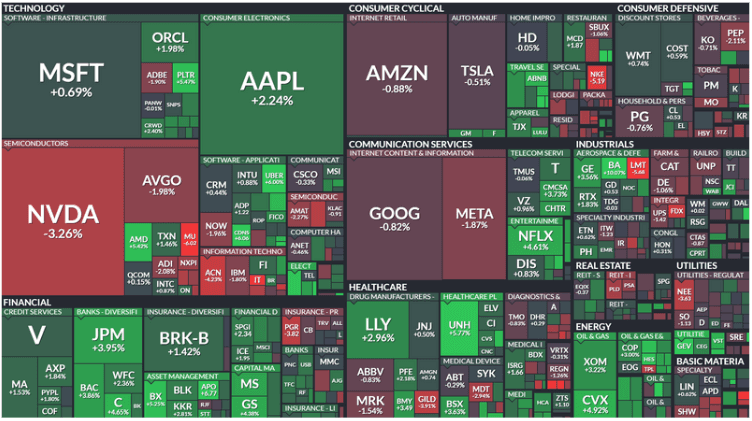

U.S. equities posted gains this week, with the Dow (+1.20%), S&P 500 (+0.51%), Nasdaq (+0.17%), and Russell 2000 (+0.63%) all finishing higher. The S&P and Nasdaq ended a four-week losing streak, though Big Tech remained mixed. Apple (+2.2%) was a standout, while Nvidia (-3.3%) lagged. Other underperformers included semiconductors, apparel, logistics, and REITs, while strength was seen in managed care, energy, asset managers, pharma, and banks. Treasuries firmed, the dollar index rose (+0.4%), gold climbed (+0.7%) for its 11th gain in 12 weeks, and WTI crude gained (+1.6%) but remained below $70 per barrel.

Corporate Highlights:

Primo Water (PRMW +47.4%): Agreed to a $1.3B take-private deal.

Guess? (GES +23.4%): Received a buyout offer from WHP Global.

Boeing (BA +10.1%): Reportedly awarded a $20B+ fighter jet contract.

Nike (NKE -5.2%): Disappointed with revenue guidance, citing restructuring challenges.

FedEx (FDX -4.9%): Lowered full-year guidance due to macroeconomic uncertainty.

Incyte (INCY -8.8%): Dropped on weak trial data.

Sector Performance:

Outperformers: Energy (+3.19%), Financials (+1.89%), Healthcare (+1.08%).

Underperformers: Consumer Staples (-0.26%), Materials (-0.25%), Utilities (-0.21%).

Markets reacted to the Fed’s policy stance, easing trade tensions, and mixed economic data. Investors now shift their focus to next week’s PCE inflation report, consumer confidence, and key earnings from Lululemon, Paychex, and GameStop.

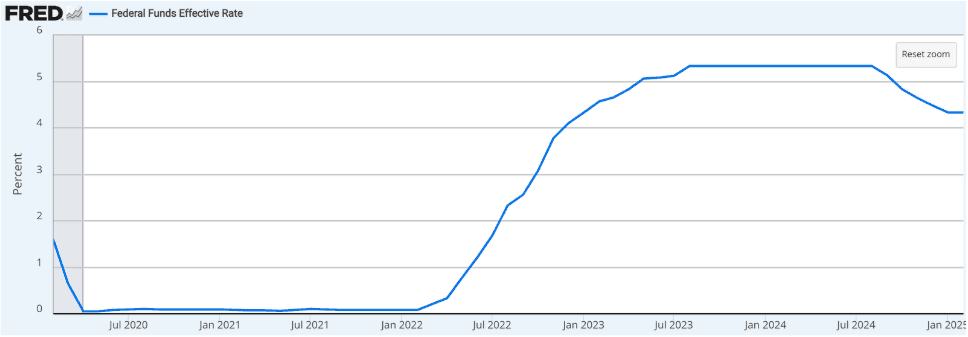

The Federal Reserve opted to keep interest rates unchanged at 4.25% to 4.5%, signaling a cautious approach amid persistent inflation and economic uncertainty. This marks the second consecutive meeting where the central bank has held rates steady following a series of cuts in late 2024. Policymakers cited increased uncertainty in the economic outlook, emphasizing their dual mandate of maximum employment and stable inflation at 2%. While the Fed’s latest projections indicate two 25-basis-point cuts in 2025, inflation remains slightly elevated, with the Personal Consumption Expenditures (PCE) index forecasted at 2.7% for the year. Fed Chair Jerome Powell acknowledged that tariffs are playing a role in rising inflation expectations but emphasized the challenge of distinguishing their impact from broader price pressures. Despite concerns over slowing growth and higher unemployment projections, Powell noted that the labor market is not currently a major source of inflationary pressure. Markets remain divided on the Fed’s next move, with a 55% probability of a rate cut in May, according to the CME FedWatch tool. However, Powell signaled that the Fed is in no rush to act, preferring to wait for more clarity on inflation trends. Investors will closely watch upcoming economic data, including the next FOMC meeting on May 6-7, for further insight into the central bank’s policy direction.

What to watch:

Notable Earnings:

Monday (3/24)

Wag! Group Co. ($PET)

Lucid Diagnostics Inc. ($LUCD)

Tuesday (3/25)

McCormick & Co. Inc. ($MKC)

Rumble Inc. ($RUM)

GameStop Corp. Cl A ($GME)

Wednesday (3/26)

Dollar Tree Inc. ($DLTR)

Chewy Inc. Cl A ($CHWY)

Petco Health & Wellness Co. ($WOOF)

Thursday (3/27)

lululemon athletica inc. ($LULU)

Friday (3/28)

Cheche Group Inc. ($CCG)

Notable Ex-Dividend Dates:

Monday (3/24)

Portland General Electric ($POR) 4.79%

Tuesday (3/25)

Altria Group ($MO) 7.40%*

Best Buy ($BBY) 4.38%

Wednesday (3/26)

Acme United ($ACU) 1.56%

Thursday (3/27)

Curtiss-Wright ($CW) 0.20%

Invitation Homes ($INVH) 3.53%

Build-A-Bear Workshop ($BBW) 2.48%

Friday (3/28)

British American Tobacco ($BTI) 7.34%

DICK'S Sporting Goods ($DKS) 2.29%

Humana ($HUM) 1.33%

*Dividend Aristocrat